Page 14 - FY 2021-2022 Audited Financial Statements

P. 14

Child Care Resource Center, Inc. Notes to Financial Statements

Note 2 – Summary of Significant Accounting Policies (continued)

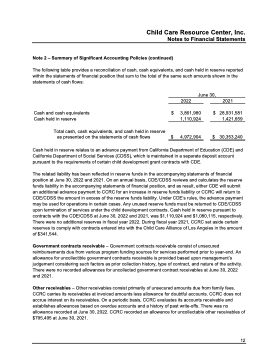

The following table provides a reconciliation of cash, cash equivalents, and cash held in reserve reported within the statements of financial position that sum to the total of the same such amounts shown in the statements of cash flows:

Cash and cash equivalents Cash held in reserve

Total cash, cash equivalents, and cash held in reserve as presented on the statements of cash flows

June 30,

2022 2021

$ 3,861,980 $ 28,931,581 1,110,924 1,421,659

$ 4,972,904 $ 30,353,240

Cash held in reserve relates to an advance payment from California Department of Education (CDE) and California Department of Social Services (CDSS), which is maintained in a separate deposit account pursuant to the requirements of certain child development grant contracts with CDE.

The related liability has been reflected in reserve funds in the accompanying statements of financial position at June 30, 2022 and 2021. On an annual basis, CDE/CDSS reviews and calculates the reserve funds liability in the accompanying statements of financial position, and as result, either CDE will submit an additional advance payment to CCRC for an increase in reserve funds liability or CCRC will return to CDE/CDSS the amount in excess of the reserve funds liability. Under CDE’s rules, the advance payment may be used for operations in certain cases. Any unused reserve funds must be returned to CDE/CDSS upon termination of services under the child development contracts. Cash held in reserve pursuant to contracts with the CDE/CDSS at June 30, 2022 and 2021, was $1,110,924 and $1,080,115, respectively. There were no additional reserves in fiscal year 2022. During fiscal year 2021, CCRC set aside certain reserves to comply with contracts entered into with the Child Care Alliance of Los Angeles in the amount of $341,544.

Government contracts receivable – Government contracts receivable consist of unsecured reimbursements due from various program funding sources for services performed prior to year-end. An allowance for uncollectible government contracts receivable is provided based upon management’s judgement considering such factors as prior collection history, type of contract, and nature of the activity. There were no recorded allowances for uncollected government contract receivables at June 30, 2022 and 2021.

Other receivables – Other receivables consist primarily of unsecured amounts due from family fees. CCRC carries its receivables at invoiced amounts less allowance for doubtful accounts. CCRC does not accrue interest on its receivables. On a periodic basis, CCRC evaluates its accounts receivable and establishes allowances based on overdue accounts and a history of past write-offs. There was no allowance recorded at June 30, 2022. CCRC recorded an allowance for uncollectable other receivables of $795,495 at June 30, 2021.

12